Crude markets remain volatile as prices respond to rapidly shifting geopolitical headlines, winter‑related supply disruptions, and evolving global trade dynamics. After a sharp selloff earlier this week as Middle East tensions appeared to ease, crude prices have since stabilized and edged higher as new geopolitical incidents revived risk concerns.

The recent pullback was driven by a removal of geopolitical risk premium, with traders temporarily shifting focus back to supply‑demand fundamentals. That calm proved short‑lived. Reports of U.S. naval action involving an Iranian drone and heightened activity near key shipping lanes quickly rebuilt risk premium, highlighting how sensitive the market remains to geopolitical developments.

On the supply side, OPEC+ confirmed it will maintain current output levels into March, delaying previously planned increases. This decision reflects caution around early‑year demand softness and uneven global economic conditions, while also providing a floor under prices.

In the U.S., production and refinery operations continue to recover from recent winter storms. While some crude output has returned, refinery restarts remain uneven due to power and mechanical issues. This has kept refined product markets—particularly distillates—tighter than crude.

Diesel remains the standout strength, supported not only by traditional heating demand but also by non‑transport usage. Extreme cold has driven fuel‑switching in power generation, especially in regions like New England, where distillate can substitute for constrained natural gas supply.

Globally, crude flow patterns are increasingly driven by economics rather than diplomacy. Indian refiners have continued to favor discounted barrels despite pressure to reduce Russian imports. However, a newly announced U.S.–India trade agreement has shifted sentiment, signaling a gradual move away from Russian crude toward U.S. and Western Hemisphere supplies. That transition is expected to be phased and uneven due to refinery configuration constraints and pre‑booked cargoes.

Meanwhile, the Russia–Ukraine conflict and ongoing sanctions enforcement continue to underpin a structural price floor. While broader fundamentals point to gradual inventory builds over the medium term, geopolitical risks remain the dominant driver of short‑term price swings.

Market Outlook

Looking ahead, markets are likely to remain headline‑driven in the near term, with volatility elevated as geopolitical risk periodically re‑enters pricing. The Strait of Hormuz and broader Middle East security will remain critical flashpoints for crude risk premium.

Crude prices may face downside pressure if geopolitical tensions ease again and refinery operations normalize more quickly than expected. However, OPEC+ restraint, uneven global supply recovery, and persistent sanctions risk limit the scope for sustained downside.

Refined products—especially diesel—are expected to remain relatively firm through the remainder of winter. Cold‑weather demand, fuel‑switching dynamics, and delayed refinery normalization suggest distillate balances will stay tighter than crude or gasoline.

Over the medium term, shifts in global crude flows—particularly India’s gradual reallocation away from Russian barrels—could reshape regional differentials and support U.S. export demand. That adjustment is likely to unfold over months rather than weeks, creating intermittent pricing dislocations rather than a smooth transition.

Bottom line: fundamentals point to a cautious, range‑bound crude market, but geopolitical risk and winter‑driven product tightness continue to skew outcomes toward volatility rather than stability.

If you have any questions or would like current pricing, please contact your Energy Account Manager.

Propane

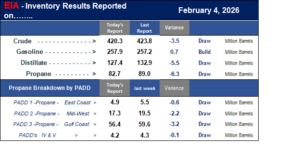

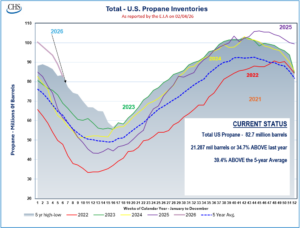

U.S. propane inventories posted a significant draw, with the EIA reporting an overall decline of 6.3 million barrels. The bulk of the draw occurred in the Gulf Coast (3.26 million barrels) and the Midwest (2.2 million barrels). This draw reflects strong, widespread demandacross much of the country, particularly in the Gulf Coast, East, and Southeast regions, combined with lower production levels.

Freeze-off impacts are evident in current production data, though they are less severe than those experienced in 2021 or 2023. Historically, production tends to recover relatively quickly following freeze-off events.

Adding to near-term supply constraints, an operational issue at the Energy Transfer–operated LPG export docks in Nederland, Texasis expected to limit LPG exports for the first 10–12 days of February.

Market Outlook

Near-term propane market fundamentals remain supportive, driven by continued seasonal demand and temporarily reduced production tied to freeze-offs. While freeze-related disruptions are expected to ease, inventory levels have already been tightened by recent draws.

The short-term curtailment of LPG exports from Nederland, Texas, may provide some relief to domestic supply, potentially moderating the pace of inventory draws in early February. However, once operations normalize, export demand could reassert pressure on balances if strong domestic demand persists.

Overall, the market is likely to remain sensitive to weather-driven demand and production recovery timing in the near term, with price direction closely tied to how quickly supply rebounds relative to ongoing consumption.

If you have any questions or would like current pricing, please contact your Energy Account Manager.

NuWay-K&H Cooperative Customer Portal

Through our portal, you can check billing, make payments, request a quote, check previous years product usage, see invoices and statements, and much more. We also offer digital contracting through the portal where you can sign and pay your energy contracts through our mobile app or desktop site. Click here to log in!